© 2025 Onward. All rights reserved.

Designed by BX Studio

Plug in your sources, clean your data, and watch performance marketing soar—flat fee, zero drama. Get started with a discovery call.

The fastest way to calculate contribution margin is to subtract your variable costs from your revenue. It matters because it shows how much money you keep after each sale. The main risk is misclassifying costs, which distorts every decision that follows.

TLDR

Most teams use ROAS because ad platforms hand it to them. The problem is that ROAS ignores the real economics of the product. It does not include cost of goods, fulfillment, discounts, return handling, or payment fees.

{{video}}

Without margin clarity, operators scale campaigns that look good in a dashboard but lose money once true costs are included.

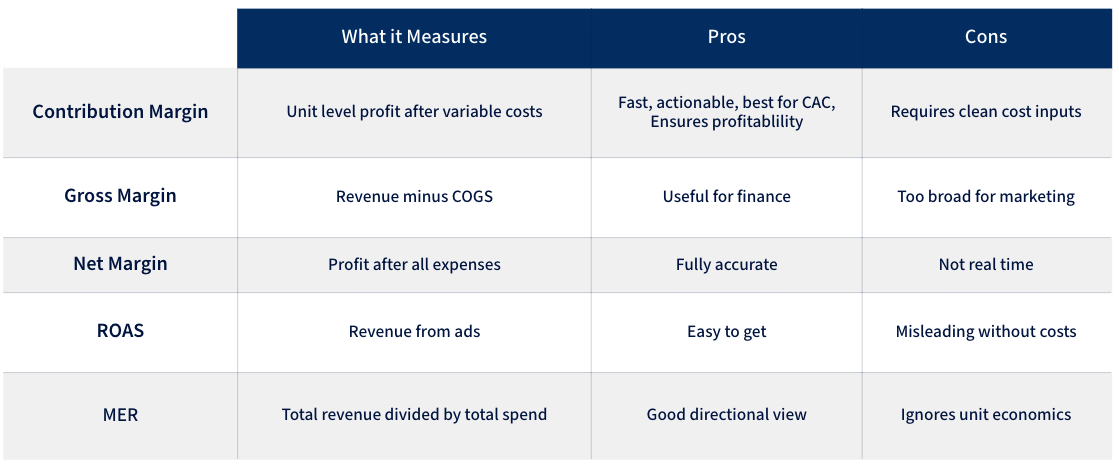

ROAS is directional. Contribution margin is operational.

Contribution margin solves the ROAS problem by showing the true dollars available after variable costs.

Contribution Margin = Revenue minus Variable Costs.

Variable costs are any costs that increase with each unit sold. Examples include cost of goods, packaging, shipping, payment fees, and returns handling.

Step 1. Start With Net Revenue Per Unit

Revenue after discounts is your true starting point.

Step 2. List All Variable Costs

Variable costs increase with volume. Typical examples:

Step 3. Subtract Variable Costs

If revenue is 30 dollars and variable costs are 18 dollars, contribution margin is 12 dollars.

Step 4. Convert to a Percentage

Contribution Margin Percentage = 12 divided by 30 equals 40 percent.

Step 5. Use Margin to Set CAC Targets

Your maximum CAC should not exceed your contribution margin unless you are intentionally breakeven for LTV expansion.

Step 6. Add LTV for Multi Purchase Models

Multiply contribution margin across expected lifetime orders.

Gross margin is too broad. Net margin is too slow. Contribution margin is fast, precise, and actionable for CAC decisions.

Subtract variable costs from revenue. If revenue is 50 dollars and variable costs are 30 dollars, contribution margin is 20 dollars, or 40 percent.

Any cost that increases with each unit sold. Common examples include cost of goods, packaging, shipping, payment fees, and fulfillment labor.

What is a good contribution margin?

Most consumer brands target 30 percent to 60 percent. Below 25 percent makes scaling difficult without strong LTV.

Your maximum CAC should not exceed your contribution margin unless you are intentionally acquiring customers at breakeven.

Quarterly for stable businesses. Monthly for fast moving brands.

.svg)